2020年房地产市场呈现出典型“低开平走、持续回升”

2020年,受疫情影响,房地产市场将呈现典型的“低开平、持续回升”特征,市场回暖态势良好。剔除疫情影响,市场整体仍以“稳”为主。一季度,房地产市场受疫情影响较深,多数指标录得同期最大跌幅。随后,随着疫情防控形势的好转和复工复产的全面推进,房地产市场快速回暖。本季度除房屋竣工面积和土地购置面积外,其他主要指标均呈正增长,基本接近或超过同期历史水平。 . 1-11月,房地产开发投资增速比固定资产投资快4.2个百分点。房地产业继续在国民经济中发挥重要支撑作用。前三季度房地产业增加值增速快于GDP增速。房地产业增加值占GDP比重7.33%,比2019年提高0.3个百分点。

在“稳”的同时,房地产市场也出现了一些典型的变化。市场分化持续,投资销售向东部发达地区和中西部省会城市集中。新开工面积回升动力较弱,仅东部地区保持小幅增长。购地意愿先升后降,地价率先高后低。部分城市房价上涨较快。 11月份,银川、唐山、徐州新建商品房价格同比上涨10%以上,深圳二手房价格同比上涨10%以上。房地产企业差异化明显,标杆企业销售情况明显好于中小企业。

展望2021年,随着宏观经济形势的不断好转,房地产政策仍将以“有房不炒”为总基调。部分热点城市房地产政策收紧,政策稳中趋紧,住房租赁市场建设加快,租购并举加快推进。从城镇化进程、城市更新模式、先行指标走势等多重因素来看,预计未来行业发展可能遇到天花板,市场整体将保持低速增长态势。

一、2020年全国房地产市场整体运行特点

2020年房地产市场将呈现出“低开平、持续回升”的典型特征。特别是二季度以来,随着国内疫情防控形势的不断好转,房企复工复产加速,市场快速回暖。除征地面积和商品房新开工面积指标外,其他主要指标均由负转正。平均房价涨幅有所上升。

1.商品房销售持续向好,增速由负转正

商品房销售率连续五年上升。 2020年1-11月,全国商品房销售率为75.4%,比2019年同期提高0.2个百分点,创七年新高,保持上行连续五年的趋势。

2.房地产投资抗跌,累计增速持续回升

3.新开工区跌幅收窄,回升动力较弱

新开工面积继续小幅下降。 2020年初,新房开工面积大幅下降。二季度以来,随着复工复产进程加快,新开工面积有所恢复,但受市场整体发展趋势影响,仍保持小幅下行趋势,回暖动力较弱。 1-11月,全国商品房新开工面积20.11亿平方米,同比下降2%。

4.房地产开发企业购地意愿下降,购地量缩水,价格上涨

房地产开发公司购买的土地数量减少,价格上涨。 1-11月,房地产开发企业累计购地20591万平方米,同比下降5.2%,较上年同期提高4.3个百分点。今年上半年。交易价格为13890亿元,同比增长1%。 6.1%,土地均价6746元/平方米,同比上涨22.5%。土地价格快速上涨的主要原因是企业的土地收购更集中在经济发达地区和大城市,导致土地交易的区域结构发生明显变化。

中国整体土地市场持续反弹。 2020年1-11月,共售出土地招拍挂79113宗,面积24.8亿平方米,同比增加7.8 %。规划建筑面积42.6亿平方米,同比增长7.9%,成交价6.81万亿元,同比-年增长 13.9%。其中,出售住宅用地24753块,8.43亿平方米,规划建筑面积19.3亿平方米,成交价5.42万亿元,住宅用地出让价格增速略快于土地总量。地价率先高后低。地价率在8月份达到顶峰,并已连续三个月下降。

土地市场区域差异加大。从土地成交面积看,除华北地区外,其他六大地域均保持增长,其中东北、华南、西北地区增长较快,增幅均在18%以上。从土地成交价格看,华中、华北地区略有下降,其余地区保持增长。其中,南方、西北和东北地区增长最快,增速超过30%。保费率方面,华东、华南、华北、西南地区保费率较高,均超过11%,西北地区保费率最低。

5.房地产贷款余额增速持续回落,企业资金来源由负转正

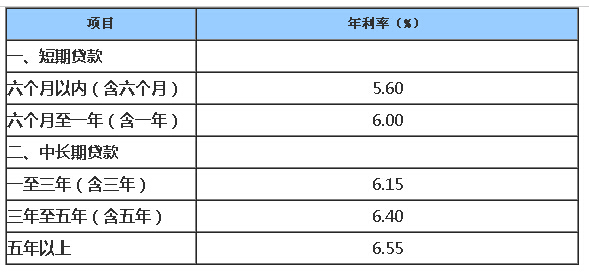

房地产贷款余额增速已连续15个季度下滑。三季度末全国房地产贷款余额48.83万亿元,同比增长12.8%,增速回落2.8个百分点,与去年同期相比。下降 0.3 个百分点。 2017年一季度以来,房地产贷款余额增速连续15个季度持续下滑。百分点。前三季度房地产贷款余额净增4.42万亿,占同期各类贷款净增的27.2%,6.@比上年同期下降>5个百分点。从房贷利率水平来看,LPR基准利率(5年期)已连续8个月锚定在4.65%,一直保持稳定。

6.平均房价涨幅有所回升,但三季度房价指数有所回落

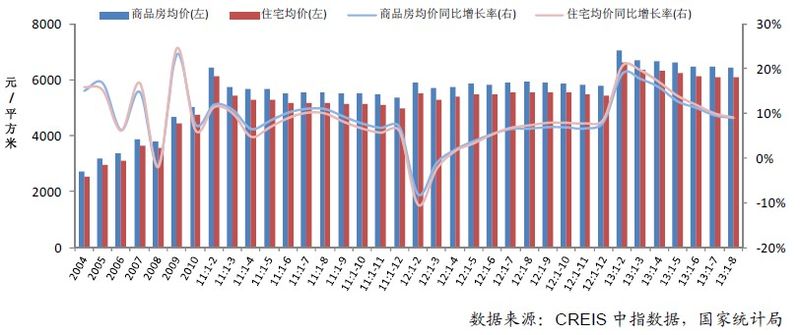

房价均价逼近万元,房价涨幅小幅上涨。从全国商品房销售均价(均价=商品房销售额/商品房销售面积,不考虑成交结构变化)来看,1-11月全国商品房均价为9876元/平方米,同比上涨5.与上年同期相比,房价上涨541元,涨幅回落1.3个百分点。但与上半年相比,房价上涨238元,涨幅2.5个百分点。

大中城市房价指数呈现回落迹象。 11月份,70个大中城市新建商品房价格环比上涨0.08%(加权平均),比10月份回落0.09个百分点;同比增长4.35%,增幅比10月份回落0.31个百分点,已连续三个月下降。

新建商品住房价格环比上涨的城市数量减少。分城市看,11月份新建商品住房价格环比上涨的城市有36个,环比减少9个,上涨城市数量明显减少; 60个城市二手房价格环比上涨,涨幅与6月份持平。受经济长期向好、人口持续流入、投资保值需求上升等因素影响,部分一二线城市二手房价格上涨压力加大,且房价上涨迹象明显。 11月,银川、唐山、徐州新建商品房价格同比上涨10%以上,深圳二手房价格同比上涨10%以上。

一、二、三线城市房价涨幅环比回落,四线城市涨幅有所回升。从新建商品房价格来看,11月,一线城市环比上涨0.2%,增速环比回落0.1个百分点,而二线城市上涨0.1%房地产市场分析指标有哪些,下跌0.02个百分点,三线城市上涨0.06%,下跌0.25个百分点,四线城市涨幅0.14%,加速0.14个百分点,一线城市涨幅最大,三线城市跌幅最大。从二手房价格来看房地产市场分析指标有哪些,一线城市上涨0.55%,二线城市上涨0.10%,三线城市上涨0.15%,第四一线城市上涨0.10%,一二三线城市下跌0.05、0.04、0.07个百分点,四线城市加速0.12个百分点。

7.标杆企业整体销售情况良好,行业集中度提高

标杆房企整体销售情况良好,行业集中度进一步提高。 2020年1-11月,39家上市房企共实现销售面积52357万平方米,同比增长13.4%,实现销售额73591亿元,同比增长11.8 %。与同期全国商品房销售面积和销售增速相比,分别快12.1和4.6个百分点。与标杆企业的销售增长形成鲜明对比的是,中小房企销售形势趋紧,压力更大。

超过 80% 的标杆企业实现销售额正增长。分公司看,22家公司销售额超过1000亿元。其中,恒大、万科、碧桂园、融创占据第一梯队,均超过5000亿元。保利、中国建筑、中国海外、世茂地产、华润置地、招商蛇口、龙湖地产、绿城中国、新城发展、金地集团、中国金茂等位列第二梯队,销售额超2000亿元。从增速看,33家企业保持增长,其中绿城中国、合生创展增速较快,均超过50%。 6家企业销售额同比下降,其中绿地香港、深圳控股、首创置业、新城发展等4家企业销售额下降幅度超过10个百分点。

二、区域楼盘情况

从区域来看,疫情冲击下的房地产市场加速分化,区域间差异更加明显。

1.华北、华东、西北地区房屋销售增长较快,华中、东北地区继续负增长

河北、江苏、浙江及西北地区部分省份销售面积快速增长。分省市看,1-11月,20个省市商品房销售面积呈现正增长,其余11个省市继续下降。具体来看,河北、江苏、浙江、山西、贵州及西北大部地区销售面积保持增长,其中甘肃、新疆、宁夏增长较快,超过10%。在下降的11个省市中,西藏、湖北、吉林、黑龙江、海南、天津下降幅度较大,均超过10个百分点。从绝对值看,江、浙、粤、河北、贵州、山东、甘肃、湖南等省商品房销售面积同比增长200万平方米以上。上年同期。湖北、吉林、黑龙江、天津等省市销售面积大幅下降,超过200万平方米,尤其是湖北省,同比减少2073万平方米。

西北、华东、华北销售情况较好。从四大区域看,东部和西部地区保持增长,分别增长5.3%和1.9%,而中部和东北部地区销量继续下滑,分别下降 3.3% 和 3.。 @7.5%。分七个地理区域来看,西北、华东、华北区域增幅较大,分别为6.6、5和4.6个百分点。东北和华中地区降幅较大,分别下降7.5和7.2个百分点。

2.房地产投资西强东稳,西北地区增速最快

90%的省份投资保持正增长。分省市看,28个省、市、自治区房地产投资实现正增长,其中西藏、新疆、贵州、吉林、内蒙古、陕西、山西、四川、上海等9个省市增长较快超过 10%。受疫情和政策影响,湖北、天津、重庆投资继续下降,但降幅均收窄,均在10个百分点以内。

西部投资强东部稳弱,华东投资占比近40%。划分为四大区域,各区域均保持正增长,呈现出“西部强东稳中弱”的特点。其中,西部地区投资增速最快,增幅8.3%,东部地区次之,增幅7.4%。中部地区相对薄弱,增幅3.6个百分点。从七大地理区域来看,华中地区投资增速依然最低,增幅1.9%,而西北、西南、华东、华南地区增速较快,均超过 7%。

3.地区新开工面积差异较大,华北、华东、西北保持增长

不同省份的新开工趋势存在显着差异。 31个省市中,14个保持增长,17个下降。 14个增长省份中,新疆、北京、浙江、山西增速最快,增幅为50.4、44、28.5、17.6个百分点,其余9个省份保持个位数增长。下降的17个省份中,西藏、贵州、天津下降超过20个百分点,海南、四川、重庆、河南、山东下降超过10个百分点。不同省市具有明显的差异化特征。

东部地区跑赢大盘,中部和西南地区跌幅超过 10%。从四大区域来看,东部地区表现突出,保持小幅增长,其余三个地区保持下降。七大地理区域中,西北地区增速最快,增速9.1%,其次是华北地区,增速5.9%,华东中国地区增长率为 2.9%。其余4个地区继续下降,其中西南和华中地区降幅较大,分别下降12.9和10个百分点。

4.华东地区房价涨幅较快,其次是西北、东北、华南

8个省市房价过万元,5个省市房价均价下跌。 1-11月,各省市商品房销售均价出现波动,26个省市保持上涨,5个省市下降。其中,西藏、上海、宁夏、浙江等四个省市房价涨幅均在10%以上,黑龙江、重庆、新疆、贵州、广西等省市房价均价下跌,均在5%以内。个百分点。从绝对价格看,平均房价超过万元的省市有8个,均位于东部地区,房价低于7000元的省市有8个,河南、湖南除外。位于西部地区。

华东地区的平均房价涨幅最高。分四大区域看,各地区房价均价持续上涨,其中东部地区涨幅最快,平均涨幅为7%,中部地区涨幅最慢,平均涨幅为7%。 2%。划分为七个地理区域,除华中略有下降外,其他区域均上涨。其中华东地区涨幅最大,同比涨幅8.4%,其次是西北、东北、华南,分别上涨6.1、< @4.7、4.6 个百分点。

5.区域投资和销售继续分化,重点城市群差异显着

区域分化持续,长三角地区投资销售繁荣,京津冀指标分化,川渝地区增速低于全国平均水平。 1-11月,四个直辖市中,北京、上海投资和商品房销售保持增长,天津、重庆均保持下降。从四大城市群看,长三角地区投资销售两旺;珠三角地区投资保持较快增长,但销售额与全国平均水平基本持平;京津冀地区投资缓慢,但销售情况良好;四川和重庆的投资销售增速低于全国平均水平。其中,长三角地区(上海、江苏、浙江、安徽)共完成房地产投资33495亿元,同比增长7.8%,实现销售面积3.227亿平方米,增长6.8%;珠三角地区(广州、深圳、东莞、惠州等9个城市)实现投资11327亿元,增长8.9%,销售面积7344万平方米,增加 1.4%。京津冀地区(北京、天津、河北)完成投资10412亿元,同比增长2.4%,实现销售面积6786万平方米,同比增长< @4.3%。川渝地区(四川、重庆)完成投资10635亿元,实现销售面积16752万平方米,分别增长5.9和0.6个百分点,增速低于全国平均水平。

三、2021年影响房地产市场走势的主要因素

2021年是“十四五”开局之年,是我国全面建设社会主义现代化新征程的开端。加快构建以国内大循环为主体、国内国际大循环相互促进的新发展格局。中华民族伟大复兴与世界百年未有之大变局交织在一起。面对复杂严峻的外部环境,既要保持战略重心,做好自己的事情,房地产市场也要有“稳”和“变”。从“稳”看,“住不炒”仍是主基调,“以城施策”仍是地方政府发挥主体责任的主要手段,整体政策环境和市场基调依然不变稳定的。从“变”看,房地产分化进一步加剧,中央对住房问题更加重视,租购并举将加快推进。

1.新发展阶段的房地产行业需要在更高的层次上服务整体发展

2021年是“十四五”开局之年,是我国进入新发展阶段的关键节点。十九届五中全会公报指出,要统筹兼顾中华民族伟大复兴和世界百年未有之大变局,深刻认识新特点新要求我国社会主要矛盾的变化所带来的变化,深刻认识了复杂的国际环境。面对新矛盾新挑战,增强机遇意识和风险意识,立足社会主义初级阶段基本国情,坚持战略定力,把好自己的事情办好。在房地产方面,公报提出“促进金融、房地产和实体经济均衡发展”,“坚持房子是用来住的,不是用来炒的,租买兼用的定位,按照政策执行切实增加保障性住房供应,完善土地出让收入分配机制,探索支持利用集体建设用地建设租赁住房。配合规划,完善长租政策,扩大保障性租赁住房供应。”这为我国房地产未来五年的发展指明了方向。方向上,“均衡发展”、“房不炒”、“租购并举”、“增加保障性住房供应”等关键词将成为今年房地产市场发展的重点。 “十四五”,房地产要在更高水平上为发展服务。大图。

2.“有房不炒”的定位决定了房地产市场的基本面

2020年上半年,受疫情影响,各地政府从供给端和需求端推出多项政策,促进房地产市场回暖,如降低预售条件、降低预售监管资金留存比例或使用标准、土地转让资金延期分期付款、纳税延期、降低人才落户购房门槛、提供购房补贴等,楼市政策呈现宽松趋势。同时,中央层面继续坚持“有房不炒”的定位,落实城市主体责任,落实稳地价、稳房价、稳预期的长远目标。下半年,面对以长三角、珠三角为首的部分城市房价过快上涨,中央政治局重申“有房不炒” ”,明确坚持不把房地产作为短期拉动经济的手段,住建部也两次召开房地产工作座谈会,坚持稳地价原则、房价、预期,并根据城市实施差异化调控政策。金融监管部门从宏观层面加强房地产金融审慎管理,加快推进房地产调控长效机制,提升热点城市调控力度。

展望2021年,房地产政策仍以稳为主,长期坚持“有房不炒”的定位,也决定了2021年房地产市场的基本行情,不会有明显的增长或下降。从资本看,随着国内经济的持续复苏,2020年货币政策将弱于2020年,社会融资增速将低于2020年。同时,新“三红”试行近半年的“线路”将从2021年1月1日起全面实施,这将成为房地产企业盲目扩张的重要制约因素。 2021年的金融政策环境将比2020年收紧,但个人消费方面将保持相对稳定。同时,以人为核心的新型城镇化不断推进,中心城市和城市群引领作用不断增强,现代都市圈建设加快推进,保障性住房建设和供应将再度提速这些因素将支撑房地产市场的稳定增长。有较大的波动。总体来看,房地产市场仍以稳定为主,“租购并举”和“租购同权”将成为未来市场的重要方向。

3.大城市成为2021年房地产市场的重要焦点和增长点

根据国内外经济发展规律,人口趋向于明显的中心城市和城市群,这也是大城市住房问题较为突出的重要原因。今年中央经济工作会议特别提出“解决大城市住房突出问题”,既是对当前突出问题的问题导向应对,也是立足目标,着眼高质量发展要求的长远思考。方向。

根据相关数据,目前我国有91个特大城市,其中特大城市6个,特大城市9个,I类大城市13个,II类大城市68个。 2019年,这91个主要城市的房地产投资、商品房销售面积、商品房销售量占全国的69.3、57.5和70%,分别是我国房地产市场规模最大的。骨干。但从这91个城市的房价水平来看,均高于全国平均房价水平。据数据测算,2019年特大城市商品房均价为19019元/平方米,特大城市13480元/平方米,I类城市12058元/平方米,分别为2.0全国平均房价。 4、1.45 和 1.30 次。 Housing prices in these cities have also risen significantly faster than the national average, and housing conflicts have become more prominent. Compared with 2010, the average housing prices in megacities, megacities and I-type megacities rose by 94.1%, 105.6% and 90.3% respectively, all faster than During the same period, the national average price increase of 85%, especially in 9 megacities, was 20.6 percentage points faster than that of the whole country.

High housing prices, difficulty in renting a house, and market chaos have become important factors restricting the high-quality development of the housing sector in big cities. In terms of the type of population flow, 54 of the 91 large cities belong to the type of net population inflow, especially among the 28 cities with a permanent population of more than 3 million in urban areas, only 2 cities are of the type of population outflow, and the remaining 26 cities are of the type of population outflow. All cities belong to the typical net inflow type, and the housing problem is also the most prominent, which will be an important focus of the real estate market in 2021.

In terms of control ideas, in addition to adhering to the previous price control, it is expected that more attention will be paid to the construction of affordable rental housing, land supply will be tilted towards rental housing construction, collective construction land and idle land owned by enterprises and institutions will also be actively explored Construction of rental housing. In terms of equal rights to rent and purchase, the level of equal rights for renters to enjoy public services will be gradually improved, and the long-term rental market will be regulated.

4.Some leading indicators indicate the possibility of a steady decline in the property market

my country's urbanization process has entered the middle and late stage, and the newly added permanent population in cities and towns has been declining for four consecutive years. At present, my country's urbanization process has entered the middle and late stage, and the scale of new urban population will slowly decline. In 2019, the new permanent resident population in cities and towns was 17.06 million, which has been declining for four consecutive years, with an average annual decline of 6.16%. It is expected that the net increase of urban population is still likely to keep falling in the future. As an important part of real estate demand, the process of urbanization will directly affect the overall size of the market.

Leading indicators such as land acquisition and newly started construction area continued to decline slightly. Judging from the two leading indicators of newly started area and land acquisition area, the land acquisition area reached its peak in 2011, and has maintained a fluctuating downward trend in recent years. The newly started area of commercial housing reached a periodic peak in 2013, and then fell below the peak level for four consecutive years. Until 2018 and 2019, due to the dual influence of policies and the market, the scale of newly started area reached a new high. However, the current environment that supports the growth of new housing starts has changed. In particular, the new regulatory policy of "three red lines" will basically end the rapid turnover business model of enterprises, and the willingness of enterprises to start new construction will be affected. It is expected that new housing starts will be Keep falling back.

The urban renewal model has changed from "demolition and building new" to "functional improvement". During the "13th Five-Year Plan" period, the transformation of shanty towns, as the focus of affordable housing construction, is an important factor supporting the rapid growth of the entire real estate market. With the basic completion of the "destocking" task and the in-depth progress of the urbanization process, the transformation of shanty towns has begun to transform into the transformation of old communities. Different from the "expropriation-demolition-construction" model of shantytown renovation, the renovation of old communities is to improve community support, childcare, medical care, etc. The level of public services, improve the living conditions of residents, and build a community governance system of "vertical to the end, horizontal to the edge, co-construction, co-governance and sharing". The renovation of old urban communities will not only not generate housing demand, but will attract some housing demand due to the improvement of the living environment of the community, which will crowd out the newly built housing market.

Combining the above factors, the overall real estate market may face a "ceiling", but the development coordination and balance between the real estate industry and other industries in the national economy will be enhanced.

四、2021 Real Estate Market Outlook

In 2021, with the normalization of epidemic prevention and control and the continuous advancement of vaccine research and development, the real estate market will gradually get rid of the impact of the epidemic and maintain a steady growth trend. Affected by the unilateral upward trend of real estate in 2020, the real estate market indicators in 2021 will show the trend of "high before and at the bottom, and monthly decline". According to the relevant forecast model, combined with the current economic situation and the trend of real estate policies, it is expected that the real estate market will maintain steady growth in 2021, mainly in single digits, and some indicators will drop slightly. The main indicators are predicted as follows:

表格

2 2020-2021

Prediction of main indicators of real estate for the whole year

Unit: 100 million yuan, 10,000 square meters

1.The sales area of commercial housing declined slightly

In 2021, under the background of steady economic recovery, rigid demand and improvement demand will continue to be released steadily, but the degree of release will slow down. In addition, the real estate sales area base will show a trend of low and high in 2020. Therefore, in 2021 The year-on-year growth rate of real estate sales area is likely to show a trend of "high before and then low". At the same time, "housing and not speculating" further curbs the demand for investment housing. The improvement of the rental market and the promotion of the same right to rent and purchase have also made demanders more rational, and the possibility of a slight decline cannot be ruled out. On the whole, it is expected that in 2021, the sales area of real estate nationwide will drop slightly by 0.7 percentage points, and sales will maintain a slow growth rate of 5.1 percentage point.

2.The growth rate of real estate investment will reach about 4%

As the domestic epidemic is effectively controlled and the impact of the epidemic on the real estate market is further reduced, real estate investment will maintain steady growth. On the one hand, the inertia of investment in projects under construction and the acceleration of affordable housing construction will form a strong support for real estate development investment. On the other hand, the new "three red lines" financing regulations that will be fully implemented in 2021 will increase the financial pressure of real estate companies, and companies will be more cautious in acquiring land. The slight decline in land acquisition and new construction area in 2020 also indicates that next year Investment growth will slow down. It is expected that real estate investment will grow by 3.9% in 2021, down 2.4 percentage points from 2020.

3.The overall house price remained stable and rose slightly

Since the central economic work conference at the end of 2016 first proposed the positioning of "houses are for living, not for speculation", the local government has strictly implemented the main responsibility of real estate regulation and implemented the measures of "policy based on the city". Precise regulation has been implemented, and the increase in housing prices has been effectively controlled, and housing prices have maintained single-digit growth in most years. With the "14th Five-Year Plan" proposal and the Central Economic Work Conference's successive emphasis on "housing, not speculating," the real estate market is expected to be more clear. The overall national housing price has remained basically stable, maintaining a narrow range of fluctuations and a slight upward trend. It is expected that the national overall housing price The increase is around 5%. At the same time, with the further intensification of the regional differentiation of real estate, the differentiation of housing prices will become more obvious. Cities and regions with continuous population inflow, sufficient economic development potential and obvious transportation advantages still have upward pressure and maintain rapid growth, but those cities and regions with continuous population outflow, Areas with insufficient economic development potential, remote traffic locations, and excessive early-stage increases may have house price adjustments, so we need to be alert to the risks brought about by the inertial decline in urban house prices.

4.The regional differentiation of the real estate market further intensifies

As my country's urbanization process enters the middle and late stages, the size of the urban population will bid farewell to unilateral growth and enter the stage of the game of stock. Urban competitiveness and attractiveness will become important factors driving population flow. With the implementation of the regional development strategy and the construction of a new pattern of land and space development and protection, the economy and population will further agglomerate in urbanized areas, and the leading role of central cities and urban agglomerations will become more prominent. Adequate employment space, good public services, and convenient transportation have become the key factors in absorbing the population and supporting the continued prosperity of the real estate market. Structural demand differences in the real estate market will be further reflected. The Yangtze River Delta and Pearl River Delta regions with strong economic resilience and population mobility will perform better and maintain growth, but some regions with significant population outflow may experience negative growth. Specifically, it is expected that the Yangtze River Delta, Pearl River Delta, Beijing-Tianjin-Hebei, Chengdu-Chongqing and other urban agglomerations and surrounding key metropolitan areas will have better development, and other regions need to pay more attention to the risk of over-adjustment of the real estate market.返回搜狐,查看更多